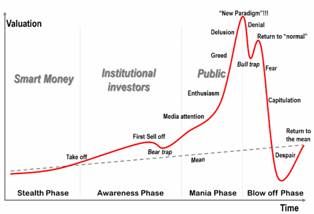

Bubbles (financial manias) unfold in several stages, an observation which backed up by 500 years of economic history. Each mania is obviously different, but there are always similarities; simplistically four phases can be identified:

Stealth. Those who understand the new fundamentals realize an emerging opportunity for substantial future appreciation, but at a risk since their assumptions are so far unproven. So the "smart money" gets invested in the asset class, often quietly and cautiously. This category of investor tends to have better access to information and a higher capacity to understand the wider economic context that would trigger asset inflation. Prices gradually increase, but often completely unnoticed by the general population. Larger and larger positions are established as the smart money start to better understand that the fundamentals are well grounded and that this asset class is likely to experience significant future valuations.

Awareness. Many investors start to notice the momentum, bringing additional money in and pushing prices higher. There can be a short-lived sell off phase taking place as a few investors cash in their first profits (there could also be several sell off phases, each beginning at an higher level than the previous one). The smart money takes this opportunity to reinforce its existing positions. In the later stages of this phase the media starts to notice with positive reports about how this new boom benefits the economy by "creating" wealth; those getting in becoming increasingly "unsophisticated".

Mania. Everyone is noticing that prices are going up and the public jumps in for this "investment opportunity of a lifetime". The expectations about future appreciation becomes a "no brainer" and a linear inference mentality sets in; future prices are an extrapolation of past price appreciation, which of course goes against any conventional wisdom. This phase is however not about logic, but a lot about psychology. Floods of money come in creating even greater expectations and pushing prices to stratospheric levels. The higher the price, the more investments pour in.

Fairly unnoticed from the general public caught in this new frenzy, the smart money as well as many institutional investors are quietly pulling out and selling their assets. Unbiased opinion about the fundamentals becomes increasingly difficult to find as many players are heavily invested and have every interest to keep asset inflation going. The market gradually becomes more exuberant as "paper fortunes" are made from regular "investors" and greed sets in. Everyone tries to jump in and new intrants have absolutely no understanding of the market, its dynamic and fundamentals. Prices are simply bid up with all financial means possible, particularly leverage and debt. If the bubble is linked with lax sources of credit, then it will endure far longer than many observers would expect, therefore discrediting many rational assessments that the situation is unsustainable. At some point statements are made about entirely new fundamentals implying that a "permanent high plateau" has been reached to justify future price increases; the bubble is about to collapse.

Blow-off. A moment of epiphany (a trigger) arrives and everyone roughly at the same time realize that the situation has changed. Confidence and expectations encounter a paradigm shift, not without a phase of denial where many try to reassure the public that this is just a temporary setback. Some are fooled, but not for long. Many try to unload their assets, but takers are few; everyone is expecting further price declines. The house of cards collapses under its own weight and late comers (commonly the general public) are left holding depreciating assets while the smart money has pulled out a long time ago. Prices plummet at a rate much faster than the one that inflated the bubble. Many over-leveraged asset owners go bankrupt, triggering additional waves of sales. There is even the possibility that the valuation undershoots the long term mean, implying a significant buying opportunity. However, the general public at this point considers this sector as "the worst possible investment one can make". This is the time when the smart money starts acquiring assets at low prices.

Bubbles can be very damaging, especially for those who arrived late with the hope of getting something for nothing. Even if they are inflationary events, the outcome of a bubble's blow off is very deflationary as large quantities of capital vanish in the wave of bankruptcies and financial defaults they trigger. Historically, they tended to be far in-between, but between 1995 and 2008 three bubbles took place back-to-back; the stock market (deflated in 2000), real estate (deflated in 2006) and commodities (deflated in 2008).

GEORGE SOROSpresented 17-04-2008:"MARKETS ARE NOT OUT OF TROUBLE YET" and his book: The New Paradigm for Financial Markets: The Credit Crisis of 2008 and What It Means. Socialism failed, communism failed and now regulations failed. It is a global thing, a not isolated and different crisis in the integrated economies on several (contradicted) levels. What we see now is a period of instability (and uncertainty). Maintaining stability has to be the objective of the authorities by a more semantic rule of regulations. Not only money supply but also credit supply and hedgefunds need to be controlled. There is a commodities bubble still in the growth phase.

Before an audience of CEPS members and guests at the Club de Warande in Brussels, George Soros, the famously successful speculator, investor, author, philanthropist and political activist, presented his latest book, The New Paradigm for Financial Markets: The Credit Crash of 2008 and What It Means, containing his views on the current financial crisis, its causes and solutions.

According to Soros, the crisis emerged with the bursting of the US housing bubble and has its origins in the dominance of the current paradigm of efficient markets, or so-called market fundamentalism or ideology. In his view, this assumption is incorrect from a philosophy of science standpoint.

Market fundamentalismassumes that markets function efficiently, move to the equilibrium, and therefore work in everyones best interest. However, contrary to the views of his mentor Karl Popper, Soros argues against the unity of science and considers economics asocial sciencethat cannot rely onnatural scienceassumptions.

Natural phenomena operate according to the law of cause and effect andhumansuse their cognitive abilities to understand. Yet, humans do not only observe but play a participative-manipulative role in social science phenomena. In terms of the market, the concept of equilibrium is a natural science theory that does not apply to economics. Specifically, Soros focuses on the concept of reflexivity, where individuals with their perception shape reality and create disequilibrium rather than equilibrium when they enter into market transactions.

This leads to uncertainty. The evidence shows that contrary to the statistical assumption of normal distribution, reflexivity leads to thick tails. In practical terms, the crisis started in the 1970s, when the oil crisis led to imbalances between oil importers and producers, which had to be covered by the banks. This resulted in a bank crisis in the early 1980s under Reagan and Thatcher, when banks were given greater freedom to cope, relying on the market to take care of it. According to Soros, the credit expansion trend towards a bubble was reinforced by the misperception of a self-correcting market, which in turn reinforced the bubble. Usually, when there are signs that a possible bubble if forming, there is a testing/twilight period.

If this test is passed, the misperception prevails and the bubble grows. If this test is not passed, policy is adapted and there is no bubble.

For the current crisis, the test would have had to be failed and the authorities would have been obliged to regulate the financial market.However, on the contrary, the test was passed and the housing bubble burst in August 2007, exposing all the accumulated weaknesses based on market fundamentalism. One of those weaknesses is that instead of financial regulation, moral hazard was created, whereby the institutions causing the financial risk were not the ones to fully bear it.The current financial crisis, which is characterised by a situation of uncertainty, liquidity shortages and solvency problems (where counter-parties cannot deliver), offers a strong argument in favour of a paradigm shift away from market fundamentalism towards more financial market regulation.

In Soros opinion, an international financial regulation agreement, for example a Basel III Accord, would be suitable. He proposes to regulate every aspect of financial market, encompassing capital, derivatives and currency markets. Soros suggests that the authorities have not understood the necessity of a paradigm shift and thereby deny any responsibility for this current crisis. Instead of regulating the financial market, for example, he expects the Fed to react in conventional ways: increase the money supply by lowering interest rates to counter the effects of the crisis until even this strategy fails.

The United States might face a recession and inflation, which might have a global impact due to the globalisation of international financial markets. He observed that the ECB had limited its actions to keeping the interest rate at 2%. There will definitely be global effects but they will affect different sectors in different parts of the world to a different degree. The prediction is that everything will be fine, it is just a question of time. Concerning the dollar as a strong or weak currency, Soros thinks that the euro will not replace the dollar as a global reserve currency and that the dollar will eventually recuperate. For the moment, there is a general flight from cash towards real assets until the dollar becomes the reserve currency again.

A Hungarian journalist proposed to Soros that he should fund the creation of modern think-tanks to research his theories and propose regulation. Soros replied that research can be like finance: the higher the risk, the higher the possible return. In other words, the more risky the theory defended, the higher the return when the theory turns out to render the best predictions.

Most of our activities in modern civilization are guided by complex financial institutions. These institutions manage the diverse psychological impulses of millions of people into a coherent whole. And yet, these institutions appear imperfect, and vulnerable to bubbles and crashes, as highlighted by the world financial crisis whose epicenter was 2008 and whose effects are still being felt today.

We are not going to turn our backs on financialcapitalism, but we do need to face squarely its imperfections so that we can minimize them. We need regulatory policies that take account of the human dimensions of these crises. We need radical financial innovations that are defined with recognition of these dimensions. We need a vision of a truly good society that hasfinancial institutionsat its base.

Prof. Shiller(*) defines a good society as a society with little violence and some degree of equality. No total absence of income inequality, because a little inequality is always necessary to let operate the society and economy. He shows a graph of the huge rise in house prices in the U.S. The increase can not be explained by interest or demographics.

A real bubble (here he gives here a friendly sneer at Eugene Fama, another Nobel Prize winner, who does not believe in bubbles) can be compared to epidemics, because people infect each other. Shiller regularly sends a survey to wealthy Americans. He asks them: do you agree with the statement that investment is the good long-term strategy? The number of people say yes, when will the stock market go up and down as prices fall. Opinions behave like a virus. People stabbing each other. This creates bubbles.

The view that financial markets are perfect as they are, and governments should not interfere in it makes this crisis so far suggests Robert Shiller, Yale economics professor and Nobel Prize winner economy in 2013.

Shiller argues that financial innovation is necessary; the development of financial principles with a social or democratic aspect which better serve the population.

Robert Shiller gave the Tinbergen lecture on the Dutch Day of Economists 2013.

The same applies to the housing market: just before the blow almost no one thought that house prices in the U.S. would fall. Through a survey with open questions about the economy, which Shiller regularly sends to 400 Americans, appears that just before the bursting of the bubble in the housing market, none of the respondents used the term bubble. After the bursting of it, just everyone talked about the bubble.

Is there a new bubble emerging in the U.S. housing market? The prices rise again, but now it's much quieter. On the Chicago's exchange, Shiller has built a futures market for single-family homes and he sees no wild movements.We need innovation in our financial sector, good innovation, so that the sector is subservient to society. In Shiller's 'good society' ordinary people suffer less from the wanted results ( epidemics ) of the financial markets.

With the advent of computers and increasing globalization, the income inequality is likely to increase significantly in the coming years. In the U.S. But also in the Netherlands. Shiller believes that we have to make plans now for what we do as income inequality increases further and not when it occurred already. The average tax rate for wealthy Dutch is now about 40 percent, says Shiller. That should be in the distant future perhaps 90 percent! (room laughs, not Shiller). 75 Percent is fine also, he says. And there should be a generous deduction for donations from rich to poor.

And then he finished. Shiller let us know now not to economize. We have to increase taxes and government spending. Then you keep people at work, without a quick rise of the debt. 'The deficit friendly stimulus'.

(*)

Professor Shiller, who has recently won the Nobel Prize in economics, is Sterling Professor of Economics, Department of Economics and Cowles Foundation for Research in Economics bij de Yale University and Professor of Finance and Fellow at the International Center for Finance, Yale School of Management.

Jean-Paul Rodrigue, Dept. of Global Studies & Geography, Hofstra University claims that stages in a bubble business cycle are a well understood concept commonly linked with technological innovations, which are often triggering a phase of investment and new opportunities in terms of market and employment.

The outcome is economic expansion and as the technology matures and markets become saturated, expansion slows down.

A phase of recession is then a likely possibility as a correction is required to clear the excess investment or capacity that irremediably occur in the later stages of an economic cycle. The bottom line is that recessions are a normal condition to a market economy as they are regulating any excess, bankrupting the weakest players or those with the highest leverage.

However, one of the mandates of central banking is to fight a process (business cycles) that occurs "naturally".

The interference of central banks such as the Federal Reserve appear to be exaggerating the amplitude of bubbles and the manias that fuel them. It could be argued that business cycles are being replaced by phases of booms and busts, which are still displaying a cyclic behavior, but subject to much more volatility. Although manias and bubbles have taken place many times before in history under very specific circumstances (Tulip Mania, South Sea Company, Mississippi Company, etc.), central banks appear to make matters worst by providing too much credit and being unable or unwilling to stop the process with things are getting out of control (massive borrowing). Instead of economic stability regulated by market forces, monetary intervention creates long term instability for the sake of short term stability.

BITCOIN

Bitcoin, a cryptocurrency and worldwide payment system and the first decentralized digital currency, as the system works without a central bank or single administrator, may now be the biggest financial bubble of all time. The cryptocurrency now looks to be bigger than any of the 10 other market bubbles it studied including the the tech bubble, beanie babies, the Dow in 1929 and the silver bubble of the late 1970s. Bitcoin was third behind an 18th-century French financing scheme around the development of the Mississippi Valley, known as the Mississippi bubble, and the one-day 31 percent surge in Qualcomm in December 1999. According to Birinyi Associates, it was a Wall Street analyst's call for a $1,000 target that set Qualcomm shares on fire. The cryptocurrency market goes beyond bitcoin, but none has appealed to the broader, general public in quite the same way. Wall Street has been late in catching up to the individual investors and cryptocurrency traders who expect bitcoin to keep surging. Three exchanges have rushed to launch bitcoin products. Futures started trading Sunday on the Cboe, with a separate contract expected to launch at the CME this weekend. Nasdaq also plans to offer futures next year.

GREENSPAN

Greenspan breaks down 'greatest global crisis ever'

In a lunchtime conversation during the Aspen Ideas Festival 2010, former Federal Reserve Chairman identified major contributing factors. I've always been in favor of the principle of sub-prime loans because I've always thought that minority homeownership in a capitalist society was highly desirable.

Greenspan did outline his belief that higher or additional taxes are an effective way to cut the national deficit but only in the short run. "The general conclusion that more people are coming to is that you cannot significantly contract fiscal problems through taxes. It will cure the deficit temporarily, but the problem is that the forces that generate it are still in play, and you'll continue to get the increase again. But if you cut spending permanently, it's a different base.

Other three financial experts gave different views on whether the financial crisis is really over. The United States has moved from recession to recovery. Now it's going to require patience to move from recovery to expansion. Fortunately, Obama realizes the problems posed by federal debt and plans to address it once the economy is stronger. The world is coming into balance thanks to the biggest global shift most people will witness in their lifetimes.